Custom Fintech Software: Build, Embed, or Adapt for Banks and Startups

Custom fintech software is a tailored financial technology platform, such as a payment system, lending engine, digital wallet, neobank application, or wealth management tool, built for a specific financial workflow, regulatory jurisdiction, or customer segment that off-the-shelf fintech products cannot serve.

Banks and funded startups approach custom fintech software from opposite directions. Banks need to modernize legacy systems, add digital channels, and maintain regulatory standing while integrating new technology. Startups need to build differentiated financial products fast enough to capture market share while meeting compliance requirements they often encounter for the first time. Custom fintech development is typically viable for teams with a development budget of $100,000 or more and a 9- to 15-month runway; teams below that threshold should evaluate BaaS or white-label paths first. This guide compares three paths to market (a fully custom build, Banking-as-a-Service, and white-label fintech platforms) and covers the compliance, integration, and partner evaluation criteria that both audiences must verify.

Atta Systems builds custom fintech software for funded startups and growth-stage companies in payments, lending, and embedded finance, with compliance-ready architecture and named-client case studies.

What custom fintech software covers

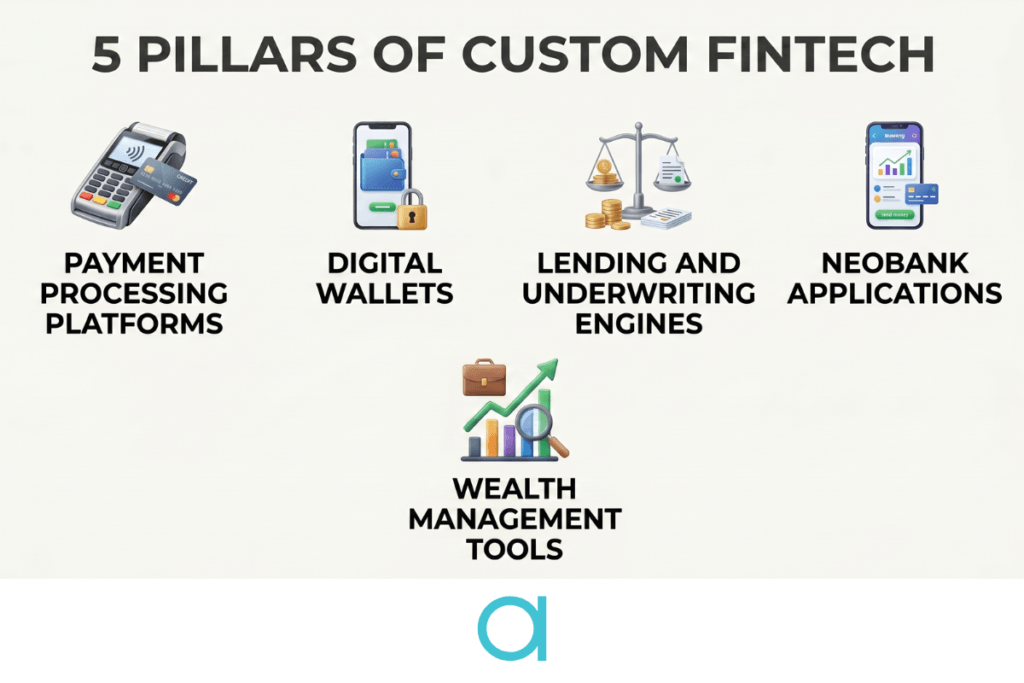

Custom fintech software spans seven product categories: payment processing platforms, digital wallets, lending and underwriting engines, neobank applications, wealth management and robo-advisory tools, insurance (insurtech) platforms, and back-office financial infrastructure, including reconciliation, ledger systems, and reporting.

Seven categories of custom fintech software:

- Payment processing platforms handle transaction routing, merchant settlement, and payment method orchestration across cards, ACH (Automated Clearing House), wire transfers, and real-time payment rails. Custom payment platforms are needed when the business requires proprietary settlement logic, multi-currency routing, or split-payment models that standard processors like Stripe or Adyen do not natively support.

- Digital wallets store, send, and receive funds in a branded mobile or web application. Custom wallet development is required when the product needs a closed-loop payment ecosystem, loyalty program integration, or peer-to-peer transfer features tied to a specific marketplace.

- Lending and underwriting engines automate loan origination, credit decisioning, risk scoring, and servicing. Custom lending platforms serve lenders with proprietary underwriting models, non-traditional data sources, or regulatory requirements specific to their lending category (consumer, SMB, real estate, or embedded lending at the point of sale).

- Neobank applications provide checking, savings, card issuance, and money management through a mobile-first interface. Custom neobank development requires a BaaS partner or bank sponsor that supplies the underlying banking license, ledger, and compliance infrastructure.

- Wealth management and robo-advisory tools automate portfolio construction, rebalancing, tax-loss harvesting, and client reporting. Custom builds serve firms with proprietary investment strategies, alternative asset classes, or client experience requirements that off-the-shelf platforms cannot accommodate.

- Insurtech platforms digitize policy management, claims processing, underwriting, and distribution. Custom development applies when the insurance product requires non-standard risk models, embedded coverage at the point of transaction, or integration with legacy policy administration systems.

- Back-office financial infrastructure includes reconciliation engines, general ledger systems, regulatory reporting tools, and audit-trail generators. Custom back-office software serves organizations whose transaction volumes, multi-entity structures, or jurisdictional reporting requirements exceed the capacity of off-the-shelf accounting and ERP tools.

Three paths to market: build custom, embed via BaaS, or adapt white-label

Custom fintech software reaches the market through three routes. A fully custom build gives complete control over financial logic, data, and regulatory submissions, but requires the longest timeline. BaaS providers like Unit, Treasury Prime, Synctera, or Atelio (FIS’s enterprise embedded finance platform, formerly Bond) supply the banking infrastructure via API while the team builds the product layer. White-label fintech platforms provide a pre-built product that the team rebrands and configures.

| Factor | Build Custom | Embed via BaaS | Adapt White-Label |

|---|---|---|---|

| Cost range | $100,000 to $500,000+ for MVP. $500K to $2M+ for full platform with compliance stack. | $50,000 to $200,000 for product layer. BaaS fees per account and per transaction on top. | $30,000 to $150,000 setup. Monthly licensing from the provider. Lower upfront, higher long-term. |

| Time to market | 6 to 18 months, depending on scope and compliance pathway. | 3 to 6 months. Banking infrastructure is pre-built. Team builds product and UX. | 1 to 3 months for configuration and branding. Fastest path to launch. |

| Customization depth | Unlimited. Every financial rule, UI element, and data flow is built to spec. | High for the product layer. Limited to the banking infrastructure layer (ledger, compliance, settlement). | Low to moderate. Branding, basic workflows, and some integrations. Core product logic is fixed. |

| Compliance ownership | Full responsibility. Team (or sponsor bank) handles all regulatory requirements directly. | Shared. A BaaS provider typically holds the banking license and handles core compliance. Team handles product-level obligations. | Mostly inherited from the white-label provider. Team handles configuration-level compliance. |

| Integration flexibility | Any integration: payment processors, KYC providers, credit bureaus, core banking, open banking APIs. | Pre-built integrations within the BaaS ecosystem. Custom integrations outside the ecosystem require additional work. | Limited to the provider’s API surface. Custom integrations often require provider cooperation. |

| IP ownership | Full source code ownership. | Team owns product layer code. BaaS infrastructure is provider-owned. | No source code ownership of the base platform. |

| Regulatory risk | Highest. The team must manage compliance directly or through a sponsor bank. | Lower. BaaS provider absorbs core banking compliance. But provider instability (e.g., the 2024 Synapse collapse) can disrupt the product. | Lowest upfront. But compliance gaps in the white-label platform become the team’s problem when regulators investigate. |

| Vendor lock-in risk | None. Team controls all systems. | High for banking infrastructure. Migrating BaaS providers means re-integrating ledger, compliance, and settlement. | High. The entire product depends on the provider’s platform and pricing decisions. |

| Best for | Funded startups building differentiated financial products. Banks modernizing core systems. Firms requiring full compliance control. | Startups needing banking features (accounts, cards, payments) without obtaining their own banking license. | Teams testing product-market fit before investing in custom development. Non-financial companies adding embedded finance. |

Building custom is the right path when the product’s financial logic is the differentiator. A lending startup with a proprietary underwriting model, a payment company with a multi-currency settlement engine, or a bank replacing its core platform all need full-stack custom development because the financial rules themselves are the product.

Embedding via BaaS makes sense when the team wants to offer banking-like features (accounts, cards, money movement) without obtaining a banking license. The provider supplies regulated infrastructure via APIs while the team builds the product experience on top of it. The risk is provider dependency: the 2024 Synapse collapse demonstrated that instability in BaaS providers can freeze customer funds and disrupt downstream products.

Adapting a white-label fintech platform is the fastest and cheapest path to launch, but it offers the least differentiation. White-label works for testing market demand before committing to a custom build, or for non-financial companies that want to add embedded finance (payments, lending, or insurance) as a feature rather than a core product.

What banks need vs what startups need from custom fintech software

Banks and funded fintech startups evaluate custom fintech software against different criteria. Banks prioritize integration with existing core banking systems, regulatory continuity, and gradual modernization of legacy infrastructure. Startups prioritize speed to market, differentiated UX, and meeting compliance requirements they have not previously managed.

| Criterion | Banks | Funded Startups |

|---|---|---|

| Primary goal | Modernize legacy systems. Add digital channels (mobile, API, real-time payments) without disrupting existing operations. | Build a differentiated financial product from scratch. Capture market share in a specific niche (lending, payments, neobanking). |

| Compliance posture | Existing compliance framework. Regulatory relationships already established. New technology must integrate without breaking existing compliance standards. | Building compliance from scratch. Need to determine which frameworks apply (AML, PCI DSS, state licensing) and build or inherit the necessary controls. |

| Integration priority | Core banking system (Temenos, Finacle, FIS). Existing payment rails. Internal data warehouses. Legacy middleware. | Payment processors (Stripe, Adyen). KYC and identity providers (Plaid, Alloy). BaaS partners. Open banking APIs. |

| Timeline tolerance | 12 to 24 months is acceptable. Procurement cycles are long. Internal approvals involve compliance, risk, IT, and business stakeholders. | 4 to 6 months MVP expected. Runway pressure from investors. Speed to market is a competitive requirement. |

| Team model | Augment the internal team with specialized fintech engineers. Retain control. Partner provides expertise, not management. | Outsource or co-build. The team may not have in-house fintech engineering. Partner handles architecture, compliance setup, and delivery. |

| Budget structure | Capex or opex allocation within the annual IT budget. Procurement requires vendor due diligence, security review, and contractual negotiation. | Seed or Series A runway. The fundraising stage constrains the budget. Every month of development burns runway. |

| Primary risk | Regulatory and reputational. A failed modernization project can trigger compliance issues, customer disruption, and regulator attention. | Runway and product-market fit. Building the wrong product or failing to meet compliance requirements burns capital and delays market entry. |

For banks, custom fintech development is typically a modernization project. The bank already has customers, regulatory licenses, and operational infrastructure. The development partner’s role is to build a digital layer (mobile banking, API gateways, real-time payment processing, or analytics dashboards) that integrates with the bank’s existing core system without disrupting it. The partner needs experience working within bank IT governance, security review processes, and extended procurement timelines.

For startups, custom fintech development is a product-building exercise. The startup often lacks in-house fintech engineering, compliance expertise, and regulatory relationships. The development partner’s role is broader: defining the MVP scope, establishing the compliance framework, building the product, and preparing the team for regulatory engagement. The partner needs experience with BaaS integrations, payment processor onboarding, and the licensing requirements specific to the startup’s target market.

Compliance, security, and integration requirements for custom fintech software

Custom fintech software faces different compliance requirements depending on the product type and jurisdiction. Payment platforms handling card data must implement PCI DSS (Payment Card Industry Data Security Standard) controls. Organizations seeking security assurance typically pursue SOC 2 (System and Organization Controls 2) reports. US-based financial institutions must maintain AML/CFT (Anti-Money Laundering/Countering the Financing of Terrorism) programs in accordance with FinCEN requirements. Products that process EU personal data must comply with GDPR obligations.

The compliance table below includes a column that most guides skip: the common vendor misstatement for each standard, along with how to verify the actual claim.

| Standard | What It Actually Covers | Common Vendor Misstatement | How to Verify |

|---|---|---|---|

| PCI DSS | Technical and operational requirements for protecting payment account data. Applies to any system that stores, processes, or transmits cardholder data. As of June 2026, PCI DSS v4.0.1 is the current version; all future-dated requirements from the v4.0 transition became mandatory on March 31, 2025. Recheck the current version periodically because the PCI Security Standards Council updates the framework on a multi-year cycle. | Vendor says: “We are PCI-compliant.” This is vague. PCI DSS compliance depends on scope: which systems, which SAQ, which assessment level. A company can be PCI-compliant for one environment and not another. | Ask for: (1) Their Attestation of Compliance (AoC). (2) Which Self-Assessment Questionnaire (SAQ) they completed, or whether they did a full Report on Compliance (RoC). (3) The scope of the assessment. (4) Whether it covers the specific systems relevant to your product. |

| SOC 2 | An examination by a CPA firm covering controls relevant to security, availability, processing integrity, confidentiality, or privacy. SOC 2 is a report, not a certification. Defined by the AICPA. | Vendor says: “We are SOC 2 certified.” SOC 2 is not a certification; it is a report. A Type I report evaluates control design at a point in time. A Type II report evaluates control operating effectiveness over a period (typically 6 to 12 months). | Ask for: (1) Whether they have a Type I or Type II report. (2) The reporting period. (3) Which Trust Services Criteria are covered (security is baseline; availability, confidentiality, etc. are optional). (4) Whether the report covers the specific services you will use. |

| AML / KYC | Anti-Money Laundering and Know Your Customer requirements. In the US, FinCEN requires financial institutions to maintain AML/CFT programs under the BSA (Bank Secrecy Act), including customer identification, suspicious activity reporting, and recordkeeping. | Vendor says: “AML-ready” or “KYC built-in.” These claims often mean the vendor integrates with a KYC API (Alloy, Plaid, Onfido) but has not built the full AML program: transaction monitoring, suspicious activity reporting, risk-based customer due diligence, and sanctions screening. | Ask for: (1) Which KYC providers they integrate with. (2) Whether they build transaction monitoring rules or only customer identification. (3) Whether they support SAR filing workflows. (4) Their experience with BSA/AML examination requirements. |

| GDPR | EU regulation governing the processing of personal data of EU residents. Applies when a fintech product serves EU customers or processes EU personal data from any jurisdiction. | Vendor says: “GDPR-compliant.” This often means they have a privacy policy mentioning GDPR, not that they have implemented data processing agreements, data residency controls, data subject access request workflows, or breach notification procedures. | Ask for: (1) Data processing agreement template. (2) Where data is stored and processed (EU vs non-EU). (3) Data subject access request handling process. (4) Breach notification procedure and timeline. (5) Data Protection Impact Assessment for your specific use case. |

Integration requirements depend on the product type. Payment platforms typically integrate with payment processors (Stripe, Adyen, Checkout.com), card issuers (Marqeta, Lithic), and payment networks. Lending platforms integrate with credit bureaus (Experian, TransUnion, Equifax), underwriting data providers, and loan servicing systems. Neobank applications integrate with BaaS providers (Unit, Treasury Prime, Atelio), card networks, and ACH and wire transfer rails. Wealth management platforms integrate with brokerage APIs (Alpaca, DriveWealth), market data feeds, and custodial systems.

Regardless of product type, teams building custom fintech software should plan for open banking API integration early. Open banking regulations such as PSD2 (Payment Services Directive 2) in the EU and Section 1033 of the Dodd-Frank Act in the US are driving the adoption of standardized account-access APIs that will affect how fintech products connect to traditional banking infrastructure.

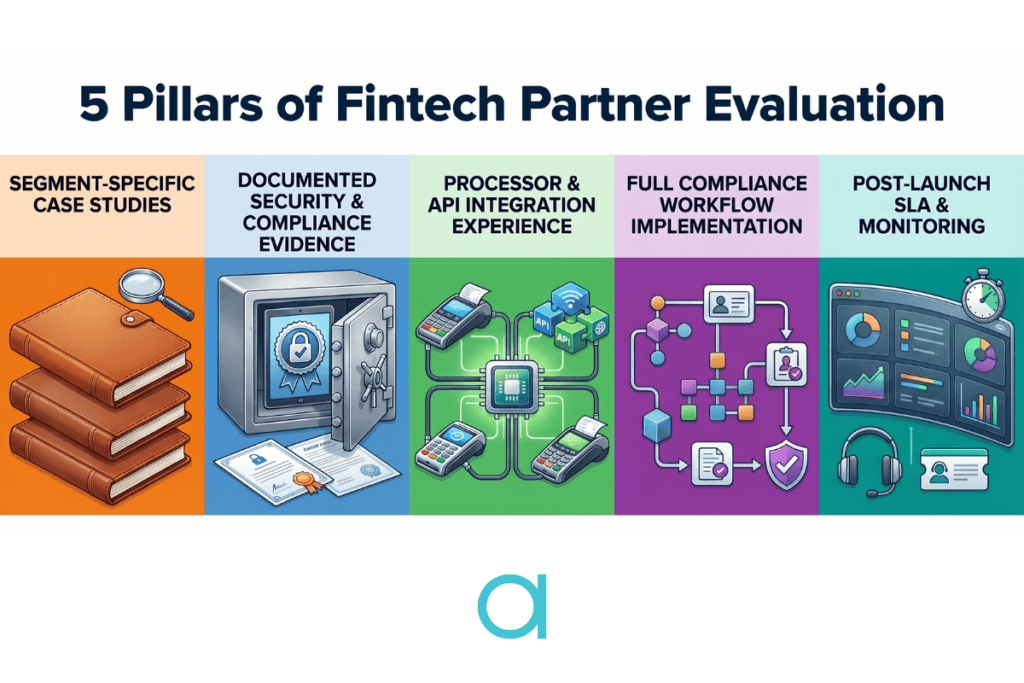

How to evaluate a custom fintech software development partner

Evaluating a custom fintech software development partner requires verifying three things: named case studies in the target fintech segment (payments, lending, banking), documented security practices with evidence beyond marketing language, and integration experience with the specific processors, KYC providers, or banking infrastructure the product requires.

Six evaluation criteria:

- Fintech segment case studies. Ask for case studies in your specific segment. A partner who built a neobank is not automatically qualified to build a lending platform. The financial logic, compliance requirements, and integration patterns differ significantly between segments. Named clients and live products matter more than “50+ fintech projects” claims.

- Security evidence. Ask for the partner’s SOC 2 report (if they have one) and their internal security practices: code review process, vulnerability management, access control, and incident response plan. If the product handles payment card data, ask about their PCI DSS experience and whether they have worked within a PCI-scoped environment.

- Processor and API integration experience. Ask which payment processors, KYC providers, BaaS platforms, or core banking systems the partner has integrated with. Fintech integrations involve webhook handling, idempotency requirements, reconciliation logic, and provider-specific edge cases that generic API developers will not anticipate.

- Compliance implementation capability. Distinguish between partners who integrate a KYC API and partners who build a complete compliance workflow: customer identification, ongoing monitoring, transaction screening, suspicious activity reporting, and regulatory reporting. The first is an API call. The second is a compliance program.

- Post-launch support and monitoring. Fintech products handle money. Downtime, bugs, or security incidents have immediate financial consequences. Ask about the partner’s post-launch SLA, monitoring setup, incident response process, and whether they provide managed infrastructure.

- Engagement model. Evaluate whether the partner offers discovery sprints for early-stage scoping, dedicated squads for full builds, and team augmentation for banks with existing engineering teams. The right model depends on whether the buyer is a startup building from scratch or a bank augmenting an internal team.

Red flags when evaluating fintech software vendors:

- “PCI-compliant” without specifying scope. PCI DSS compliance is specific to an environment and assessment level. Ask for the Attestation of Compliance and the scope. If they cannot produce it, the claim is marketing.

- “SOC 2 certified.” SOC 2 is a report, not a certification. This error indicates that the vendor does not understand the framework they claim. Request the Type II report and verify the reporting period and the covered criteria.

- “Bank-grade security.” This phrase has no defined meaning. There is no standard called “bank-grade.” Ask about the specific controls implemented: encryption standards, access management, key management, audit logging, and the frequency of penetration testing.

- “Works globally.” Fintech compliance is jurisdiction-specific. A product that works in the US does not automatically work in the EU, UK, or MENA. Ask which jurisdictions the partner has launched products in and which regulatory frameworks they have navigated.

- “Seamless integration.” Ask which specific processors, BaaS providers, or banking APIs they have integrated with. If the answer is “we can integrate with anything,” they have likely not built the reconciliation logic, webhook handling, and edge-case management that real fintech integrations require.

Atta Systems builds custom fintech software with payment processor integrations (Stripe, Adyen), KYC workflow implementation, and compliance-ready architecture, focusing on funded startups and growth-stage companies in payments, lending, and embedded finance, rather than on retail banking core systems for tier-1 banks or crypto and DeFi protocols. We also provide source code ownership from day one and offer post-launch maintenance covering security patching, AML workflow updates, and regulatory change management. This integrated approach makes us one of the game-changing app developers.

Frequently asked questions about custom fintech software

Custom fintech software costs range from $100,000 to $500,000 for an MVP to $500,000 to $2M+ for a full platform with compliance infrastructure. Building on top of a BaaS provider costs $50,000 to $200,000 for the product layer plus per-account and per-transaction BaaS fees. White-label fintech platforms cost $30,000 to $150,000 for initial setup, plus monthly licensing fees. The total cost of ownership over three years depends on transaction volume, compliance overhead, and whether the team eventually needs to migrate off a BaaS or white-label platform.

Custom fintech software development takes 6 to 18 months, depending on scope, licensing requirements, and regulatory pathway. Building on a BaaS platform takes 3 to 6 months because the banking infrastructure is pre-built. White-label configuration takes 1 to 3 months. These timelines do not include regulatory approval or licensing, which varies by jurisdiction and product type.

Banking-as-a-Service (BaaS) is a model in which a licensed bank or financial institution provides banking infrastructure (accounts, ledgers, card issuance, payment processing, and compliance) via APIs to non-bank companies that want to offer financial products. BaaS is the right choice when a startup wants to offer banking-like features (accounts, cards, money movement) without obtaining its own banking license. BaaS is not the right choice when the product requires full control over the financial logic, settlement, or compliance stack.

Whether you need a fintech license depends on your product type and jurisdiction. Money transmission in the US requires state-by-state licensing (or a single federal license if one becomes available). Lending requires a lending license in most US states. If you use a BaaS provider with a partner bank, the bank’s license covers the regulated activities, and you operate under a contractual arrangement. In the EU, a license from an Electronic Money Institution (EMI) or a Payment Institution (PI) may be required. The licensing decision should be made early because it affects architecture, compliance, and partnership choices.

Atta Systems builds custom fintech software for funded startups and growth-stage companies, covering payment processor integrations, KYC and AML workflows, BaaS architecture, and compliance-ready engineering across the product lifecycle.

Related Articles